Compliance management is what separates businesses that merely know their legal obligations from businesses that can demonstrate — to regulators, boards, and auditors — that they’re actually meeting them. It’s the operational discipline of identifying, documenting, monitoring, and evidencing compliance, consistently and systematically, across every applicable law and regulation.

For most Australian businesses, the gap isn’t knowledge of obligations. It’s the infrastructure to manage them. That infrastructure has three components: a compliance register that records what you must do, a framework that assigns responsibility and enforces accountability, and an audit process that tests whether your controls are working. This guide covers all three.

Whether you’re building your first compliance program or modernising one that’s grown unwieldy, what follows is the most practical, operational guide to compliance management in Australia available — drawn from regulatory expectations, enforcement patterns, and what actually works in practice.

What Is Compliance Management?

Compliance management is the systematic process through which an organisation identifies its legal and regulatory obligations, assigns responsibility for meeting them, monitors ongoing adherence, and produces evidence that it has done so.

That definition sounds straightforward. In practice, it requires infrastructure — documented processes, assigned ownership, regular review cycles, and an audit trail that can withstand scrutiny. Compliance management that exists only in someone’s head, or in an outdated spreadsheet, is compliance management in name only.

There are three terms that are often used interchangeably but have distinct meanings:

- Compliance management: The ongoing process of identifying, tracking, and evidencing compliance with obligations. Operational and continuous.

- Compliance framework: The structure that governs how compliance is managed — policies, procedures, roles, responsibilities, reporting lines, and escalation processes. The framework is what makes compliance management repeatable and scalable.

- Compliance program: The broader initiative that encompasses both the framework and the management activities. Often used to describe a business’s total approach to compliance as assessed by a regulator.

For context on the specific obligations your compliance management program needs to cover, see our complete guide to legal compliance in Australia.

Why Compliance Management Matters: The Regulatory Lens

Australian regulators don’t just assess whether you’ve breached a law — they assess whether you had a genuine compliance management program in place that could have prevented the breach. This distinction matters enormously at the penalty stage.

ASIC’s enforcement outcomes consistently show that businesses with documented, operational compliance programs receive more favourable treatment — lower penalties, enforceable undertakings rather than court proceedings, and greater latitude to self-report — compared to businesses that had no demonstrable compliance infrastructure at all.

The Fair Work Ombudsman’s approach to underpayment cases follows the same logic. An employer who can demonstrate a systematic payroll compliance process — even if a gap was later identified — is treated materially differently from an employer with no process and no evidence of compliance effort.

This is why compliance management isn’t just about meeting obligations — it’s about being able to demonstrate that you’ve met them, or that you’ve made genuine, documented efforts to do so. The compliance register is the document that creates that demonstration.

The Compliance Register: Your Foundation Document

The compliance register — also called a legal register, obligations register, or regulatory register — is the foundation of any compliance management program. It is a centralised, structured record of every law, regulation, licence, standard, and code that applies to your business, along with the specific obligations each creates and the evidence of your compliance with them.

A well-designed compliance register answers five questions for every obligation:

- What is the obligation? The specific legal requirement — not just “comply with the Privacy Act” but “maintain a current privacy policy, notify individuals of data collection practices, and respond to access requests within 30 days.”

- Where does it come from? The specific legislation, section, or regulatory guidance that creates the obligation.

- Who owns it? A named individual who is accountable for monitoring and evidencing compliance — not a team or a department.

- What is the current status? Compliant / at risk / non-compliant / under review — with a last-reviewed date.

- What evidence supports the status? A link to the specific document, record, or output that demonstrates compliance.

The compliance register is not a static document. It needs to be actively maintained — updated when laws change, when obligations are reviewed, when ownership changes, and when evidence is refreshed. A compliance register that’s never updated is worse than no register at all, because it creates a false sense of security.

What Goes in a Compliance Register?

The scope of your compliance register should include every obligation that applies to your business — not just the ones you’re currently focused on. For most Australian businesses, this will include:

- Corporate law obligations: ASIC reporting, director duties, record-keeping requirements under the Corporations Act

- Employment obligations: Fair Work Act minimum conditions, award obligations, superannuation, leave entitlements, record-keeping

- Privacy obligations: Australian Privacy Principles compliance, privacy policy currency, breach notification procedures

- WHS obligations: Primary duty of care, specific WHS management plans, incident notification, due diligence duties for officers

- Consumer law obligations: ACL compliance, mandatory consumer guarantees, prohibited conduct

- Tax and payroll: BAS obligations, payroll tax thresholds and lodgement, superannuation guarantee timing

- Industry-specific obligations: AML/CTF reporting entity obligations, APRA prudential standards, licensing conditions, sector-specific codes

- Licences and permits: Renewal dates, conditions, reporting requirements

- Contracts: Key contractual compliance obligations (often overlooked)

For detailed guidance on building and maintaining this document, Lahebo has published a comprehensive step-by-step guide on how to build a compliance register that covers structure, content, and ongoing maintenance in detail.

Compliance Register vs Risk Register: The Difference

These two documents serve complementary but distinct purposes. A risk register records identified risks — what could go wrong, how likely it is, how severe the impact would be, and what controls are in place. A compliance register records specific legal and regulatory obligations — what you must do, who is responsible, and the evidence that you’re doing it.

Non-compliance appears in a risk register as a risk. The compliance register is how you manage and mitigate that risk. Mature compliance programs maintain both — and link them, so that when a compliance obligation is flagged as at-risk, it surfaces in the risk register as an elevated concern requiring escalation.

Building Your Compliance Framework

A compliance register without a framework to support it is a document. A compliance framework turns that document into a program — with roles, responsibilities, processes, and accountability structures that make compliance management repeatable and scalable.

Key Elements of a Compliance Framework

Governance structure: Who oversees the compliance program? In smaller businesses, this may be the CEO or a senior manager. In larger organisations, it’s typically a dedicated compliance function reporting to the board. The governance structure defines escalation paths — what happens when a compliance gap is identified, who decides how to remediate it, and how the board receives compliance reporting.

Ownership model: Every obligation in the compliance register needs a named owner. The ownership model defines how ownership is assigned, what an owner’s responsibilities are (monitoring, evidencing, reviewing), and how ownership transfers when people change roles. The single biggest failure point in compliance programs is obligations with no clear owner, or obligations with a nominally assigned owner who doesn’t know they own it.

Review cycle: How often does each obligation get reviewed? The review frequency should be proportionate to risk — high-risk obligations (AML/CTF, WHS, privacy) warrant quarterly or even monthly review; lower-risk administrative obligations may be reviewed annually. The framework specifies the standard review cycle and defines criteria for escalating to a more frequent review schedule.

Regulatory change process: How does the organisation learn about and respond to changes in applicable law? This is a critical and commonly missing element. A compliance framework without a regulatory change process will gradually fall out of date as legislation changes — and the gap between what the register says and what the law requires will widen silently until it produces a compliance failure.

Incident and breach management: What happens when a compliance failure is identified? The framework should define a clear process: immediate containment, root cause analysis, remediation, reporting (internal and, where required, to regulators), and post-incident review to prevent recurrence.

Reporting structure: How does compliance status get reported upward? Effective compliance programs produce regular (typically quarterly) compliance status reports for senior management and the board, covering: overall compliance status, areas of elevated risk, recent incidents, regulatory changes, and upcoming obligations with significant deadlines.

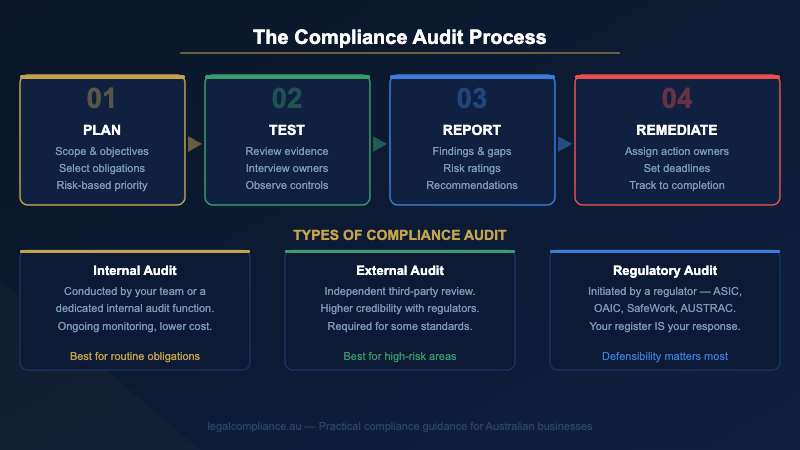

Compliance Auditing: Testing Whether Your Controls Work

A compliance register can say “compliant” for every obligation. A compliance audit asks the harder question: is that status actually true?

Compliance auditing is the systematic process of testing whether documented controls are actually operating effectively. It’s not enough to have a policy — the audit tests whether people are following it, whether the policy reflects current obligations, and whether the evidence of compliance is genuine and current.

Types of Compliance Audits

Internal compliance audits: Conducted by internal staff (not the person responsible for the obligation being audited). Internal audits are typically lower cost and higher frequency than external audits, and are most useful for monitoring high-volume, recurring obligations — payroll compliance, WHS obligations, privacy controls.

External compliance audits: Conducted by an independent third party. External audits carry more credibility with regulators and boards, and are particularly important for high-risk obligations or where internal staff lack the expertise to assess compliance accurately. APRA, AUSTRAC, and ASIC-regulated businesses typically require external audit certification for specific obligations.

Regulatory audits: Initiated by the regulator itself — ASIC, the Fair Work Ombudsman, AUSTRAC, the OAIC, or state WHS regulators may conduct audits of your business at any time. The best preparation for a regulatory audit is to run your own compliance program as if a regulatory audit were imminent at all times.

The Compliance Audit Process

A well-structured compliance audit follows four phases:

- Planning: Define the scope (which obligations will be audited), the audit methodology (document review, interviews, sampling of transactions or records), the timeframe, and who will conduct the audit. For high-risk obligations, develop a specific audit program.

- Fieldwork: Execute the audit — reviewing documents, interviewing obligation owners, testing a sample of compliance-related transactions or records, and comparing actual practice against documented procedures and obligations.

- Reporting: Produce a clear audit report covering: scope, methodology, findings (both positive and adverse), and recommendations for remediation. The report should be rated — typically red/amber/green — for overall compliance status and the severity of any gaps identified.

- Remediation: For every adverse finding, a remediation action must be assigned — with an owner, a deadline, and a process for evidencing completion. Findings without a remediation plan are findings that will recur.

Compliance Audit Frequency

The right audit frequency depends on the risk profile of the obligation and the reliability of your first-line compliance controls. As a general guide:

- High-risk obligations (AML/CTF, APRA-regulated, WHS primary duty, privacy incident response): Quarterly internal review + annual external audit

- Medium-risk obligations (Fair Work Act, privacy general obligations, consumer law): Annual internal audit

- Lower-risk obligations (administrative reporting, licence renewals): Annual review against the compliance register

- Post-incident: Any obligation involved in a compliance failure should be immediately audited, regardless of its normal cycle

Monitoring Regulatory Change: The Ongoing Challenge

The compliance register is only as current as the laws it reflects. Legislation changes. Regulators issue new guidance. Courts interpret existing obligations in ways that shift their practical scope. A compliance program without a process for monitoring and incorporating regulatory change is operating against an outdated picture of the law.

2026 is a particularly active year for Australian regulatory change. Three major changes take effect — AML/CTF Tranche 2 (1 July), payday superannuation (1 July), and the OAIC’s active privacy audit sweep — with significant implications for the compliance registers of thousands of Australian businesses. Businesses that were monitoring regulatory change were able to begin preparing for these obligations months in advance. Those that weren’t are now under immediate pressure.

Practical Regulatory Change Monitoring

A practical regulatory change monitoring process includes the following elements:

- Regulator subscriptions: Subscribe to email updates from every regulator that applies to your business — ASIC, Fair Work Ombudsman, AUSTRAC, OAIC, relevant state WHS regulator, ATO. Most regulators provide free email alerts for new guidance, enforcement releases, and legislative updates.

- Legislation monitoring: Use the Federal Register of Legislation (legislation.gov.au) to monitor amendments to key legislation. Some practices set quarterly calendar reminders to review key Acts for any recent amendments.

- Industry body membership: Industry associations often provide regulatory updates as a membership service — particularly useful for sector-specific changes that general regulatory monitoring might miss.

- Legal or compliance advisors: For businesses in heavily regulated industries, engaging an external compliance advisor or law firm for a quarterly regulatory update is a cost-effective way to capture changes that affect specialist obligations.

- Formal quarterly review: Build a formal quarterly review of the compliance register into the business calendar — specifically to assess whether any regulatory changes require updates to obligations, controls, or evidence requirements.

Compliance Management by Business Size

The principles of compliance management are the same for businesses of all sizes — but the implementation looks different depending on your headcount, resources, and regulatory footprint.

Small Businesses (Under 20 Staff)

For small businesses, the compliance register is typically the entire compliance program. The owner or a senior manager maintains a structured register of 15–30 obligations, reviews it annually (with high-risk obligations reviewed more frequently), and stores evidence in a linked folder. The key risks are incomplete obligation identification and obligations without a named owner.

Practical starting point: A spreadsheet is acceptable at this scale — but it needs to be structured (using the five-column model: obligation / source / owner / status / evidence), reviewed annually, and updated whenever a regulatory change is identified. Download a free compliance register template to get started.

Mid-Market Businesses (20–500 Staff)

At this size, a spreadsheet stops working — too many obligations, too many owners, and too much regulatory change to track manually. Mid-market businesses need purpose-built compliance management software that centralises the register, enforces ownership assignment, tracks regulatory change, and generates board-ready reporting.

The compliance framework also needs to become more formal at this stage — a documented compliance policy, a clear governance structure, and regular board reporting are expected by regulators in investigations of businesses at this size.

Enterprise Businesses (500+ Staff)

Large businesses typically have dedicated compliance functions — a Chief Compliance Officer, a compliance team, and compliance governance embedded in board committee structures. Enterprise compliance management involves complex multi-entity structures, multi-jurisdictional obligations, and integration with risk management, internal audit, and legal functions. Purpose-built GRC (Governance, Risk, and Compliance) platforms are standard at this scale.

When to Move from Spreadsheets to Compliance Software

Spreadsheets are where compliance management starts. Purpose-built software is where it scales. The transition point is typically when any of the following apply:

- You have more than 30 tracked compliance obligations

- Multiple people share responsibility for maintaining the register, creating version control issues

- Regulatory change monitoring is happening ad hoc rather than systematically

- Audit preparation requires a significant effort to compile evidence across disconnected systems

- The board or a regulator has asked for compliance reporting that a spreadsheet can’t produce

- A compliance failure has occurred that better tracking could have prevented

For Australian businesses ready to move beyond spreadsheets, Lahebo is a purpose-built compliance management platform designed specifically for the Australian regulatory environment. It centralises your obligations register, enforces ownership assignment, monitors regulatory change, and generates audit-ready reports — replacing the fragmented, high-risk spreadsheet approach with a system built for the complexity of Australian compliance.

Common Compliance Management Failures

The most common failures in compliance management programs aren’t technical — they’re structural and behavioural. Here are the five most frequently occurring gaps identified in regulatory investigations and internal audits:

1. Obligations Without Owners

The most common compliance register failure: obligations that are listed but have no named individual owner. “Compliance team” or “Legal” as an owner is not ownership — it’s diffused responsibility. Every obligation needs a person who is accountable for monitoring it, reviewing it, and maintaining evidence of compliance.

2. Stale Evidence

Evidence of compliance becomes stale — a privacy policy last updated in 2022 doesn’t demonstrate compliance with 2026 obligations; a WHS risk assessment from 2021 may not reflect current workplace conditions. Compliance programs need to define evidence refresh cycles and enforce them.

3. No Regulatory Change Process

Compliance registers are built against a snapshot of the law at a point in time. Without a systematic process for monitoring and incorporating regulatory change, that snapshot becomes progressively less accurate. The register says “compliant” — but the law has moved on.

4. Compliance Policies Without Controls

Having a written policy is not compliance. Having a written policy, a control that implements it, and evidence that the control is operating is compliance. Regulators — particularly ASIC and the OAIC — assess actual practice, not documentation. A compliance program that produces policies without ensuring they’re embedded in operational practice will fail under scrutiny.

5. Compliance Treated as an Annual Project

Compliance management is an ongoing operational discipline — not something that happens at the annual compliance review and then sits untouched for the rest of the year. Businesses that treat it as an annual project accumulate gaps between reviews that can compound into significant compliance failures by the time the next review occurs.

Frequently Asked Questions

What is a compliance register and why do I need one?

A compliance register is a centralised, structured document that records every legal and regulatory obligation applicable to your business — along with who owns each obligation, its current compliance status, and the evidence supporting that status. You need one because without a register, compliance management is entirely reliant on individuals remembering their obligations — a fragile and undefendable approach. When a regulator asks “show us your compliance program,” a well-maintained compliance register is the foundation of your answer.

How often should a compliance register be reviewed?

At minimum, the full register should be reviewed annually. High-risk obligations — AML/CTF, WHS primary duty, privacy, APRA-regulated requirements — should be reviewed quarterly. Additionally, any significant regulatory change should trigger an immediate review of affected obligations, and any compliance incident should prompt a review of the obligations involved. In practice, the best compliance programs build obligation review into regular business rhythms rather than treating it as a once-a-year event.

What is the difference between a compliance audit and a compliance review?

A compliance review typically means checking the compliance register — confirming that obligations are current, owners are engaged, and evidence is up to date. A compliance audit goes further: it tests whether the documented controls are actually operating effectively in practice. An audit involves evidence sampling, interviews with obligation owners, and an independent assessment of whether practice matches documentation. Both are necessary — reviews maintain the register; audits test whether it’s telling the truth.

Does a small business need a formal compliance framework?

Yes — though what a “formal framework” looks like for a 10-person business is very different from what it looks like for a 500-person organisation. At minimum, a small business needs: a documented compliance register (even a simple spreadsheet), named owners for key obligations, a process for reviewing the register at least annually, and a clear process for how compliance issues are escalated and addressed. The formality scales with the size and regulatory footprint of the business, but the fundamentals apply from day one.

How do I know if my compliance program is adequate?

An adequate compliance program can withstand four tests: (1) It covers all applicable obligations — identified through a systematic scope assessment, not just the obvious ones. (2) Every obligation has a named owner who is aware of and engaged with their responsibilities. (3) Evidence of compliance is current, accessible, and linked to specific obligations. (4) There is a documented process for identifying and responding to regulatory change. If your program passes these four tests, it provides a genuine foundation for defensible compliance. If it fails any of them, those are the gaps to address first.

Getting Your Compliance Management Right

Effective compliance management is a discipline, not a destination. The regulatory environment changes, obligations evolve, businesses grow into new obligations they didn’t have before, and new risks emerge as operations scale. The compliance program that was adequate last year may not be adequate today.

The businesses that manage compliance most effectively share three characteristics: they have a compliance register that is actively maintained (not filed and forgotten), they have clear ownership assigned to every obligation (not diffused across a team), and they have a systematic process for monitoring regulatory change (not relying on someone to notice when a law changes).

For businesses that are ready to move beyond a spreadsheet-based approach to compliance management — to a system that centralises obligations, enforces ownership, monitors regulatory change, and produces board-ready reporting — Lahebo is purpose-built for exactly this challenge. It’s designed specifically for Australian businesses managing compliance across multiple regulatory frameworks, and it replaces the manual, fragmented approaches that leave compliance gaps with a systematic, evidence-based program that can withstand regulatory scrutiny.